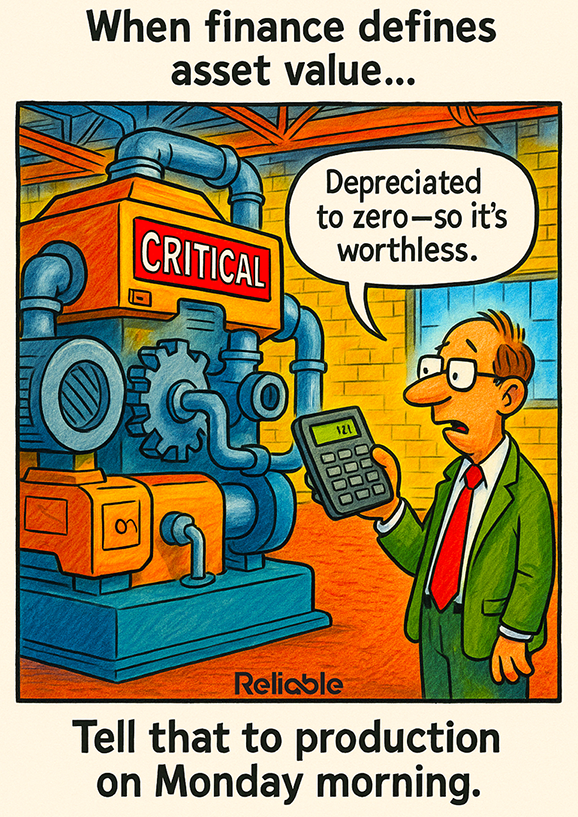

The cartoon above captures a common disconnect: finance sees a machine as worthless once it’s fully depreciated, but operations knows it’s still the heartbeat of production. This tension between accounting practices and operational realities isn’t just funny, it’s costly. To address it, we must rethink how we define “asset value” in reliability-driven organizations.

Why Asset Value in Production Goes Beyond the Balance Sheet

Depreciation is a financial construct, not a reflection of operational worth. A critical pump, gearbox, or motor may be fully depreciated, but its absence could result in millions of dollars in lost output. Traditional accounting assumes that when book value hits zero, so does usefulness – but in production, that’s absurd.

The real asset value in production comes from the economic consequences of failure. If downtime costs $10,000 per hour, a machine “worth zero” on paper could in reality be a multi-million-dollar risk exposure. Finance needs to move beyond book depreciation and account for functional value.

How Reliability-Centered Thinking Redefines Asset Value in Production

Reliability-centered maintenance (RCM) shifts the focus from accounting numbers to performance outcomes. Instead of judging an asset by its financial age, it’s judged by:

- Criticality: What happens if it fails?

- Performance: Does it meet required production standards?

- Risk Exposure: What financial and safety consequences exist?

By using a reliability-based framework, organizations can properly assess the value of their assets in production. It’s not about whether a machine has been on the books for 20 years, but whether it continues to deliver performance aligned with business goals.

This reframing also encourages proactive investment. When management understands that “zero book value” doesn’t mean “replace tomorrow,” maintenance can argue more persuasively for condition monitoring, upgrades, or redundancy strategies.

The Cost of Misaligned Perspectives on Asset Value in Production

When finance and operations misalign, three common failures emerge:

- Deferred Maintenance: If an asset is “worthless” on paper, requests for spare parts, inspections, or predictive sensors often get denied. The result: higher unplanned downtime.

- Short-Term Financial Wins, Long-Term Losses: Accounting may celebrate asset write-offs, but operations inherit instability. A machine running to catastrophic failure may incur 10 times the cost of preventive care.

- Production Disruptions: Ultimately, the asset value in production is measured by uptime and throughput. A critical asset doesn’t care what the ledger says, when it stops, everything downstream pays the price.

The real cost is cultural: engineers and reliability professionals feel undervalued when their insights are ignored in favor of accounting conventions. That erodes cross-functional trust.

Building a Unified View of Asset Value in Production

The solution isn’t to abandon financial accounting, it’s to expand the lens. Organizations can build a more unified view of asset value in production by:

- Adopting Life-Cycle Costing (LCC): Go beyond acquisition and depreciation. Include energy costs, maintenance costs, downtime costs, and disposal costs.

- Integrating Risk Analysis into Asset Registers: Criticality rankings, failure mode analyses, and downtime exposure should sit alongside financial metrics.

- Collaborating Across Departments: Finance needs to hear real downtime costs; operations needs to understand capital budgets. Bridging these silos creates better decisions.

- Updating KPIs: Instead of only tracking ROI or depreciation schedules, include metrics like Mean Time Between Failures (MTBF), cost of unreliability, and production throughput.

This holistic perspective respects the economic role assets play long after the books declare them “worthless.” It enables finance to make smarter capital allocation decisions and empowers maintenance to justify investments in reliability.

Rethinking Asset Value for Real-World Production

The cartoon effectively conveys the absurdity: labeling a critical production asset “worthless” because it has been depreciated overlooks reality. Finance may focus on balance sheets, but operations lives in the world of uptime, throughput, and risk. Asset value in production cannot be reduced to accounting entries, it must be defined by the role assets play in sustaining safe, efficient, and profitable operations.

By reframing asset value through reliability, companies align financial perspectives with operational reality, reduce downtime risk, and make smarter long-term decisions. The next time someone says an asset is “worth zero,” remind them of its real value: the cost of losing it.