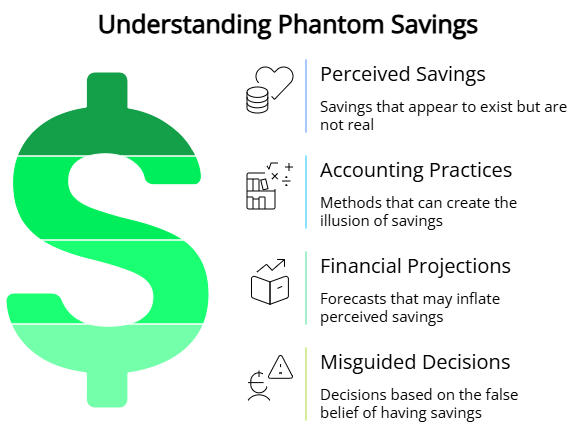

There are real cost savings, and there are phantom savings. Real cost savings are reflected in the accounting system and appear on the balance sheet. Phantom savings appear in reports and cannot be traced explicitly to the accounting books.

Some Examples of Real Savings

- Reductions in payroll (personnel)

- Non-replacement of personnel because we don’t need them

- Reduction to overtime

- Reduction to billing from contractors

- Reductions to material used

- Reductions to inventory on shelf

- Reduced expenditures for tools and equipment

- Reduced equipment rental bills

- Reduced demurrage (rental of tanks, rail cars, ships)

- Reduction of regulatory fines

- Closing a satellite operation and reduction of overhead

- Reduction of energy usage (large enough to be read)

- Reduced raw material usage (increased yield or reduced scrap)

- Reduced number of production machines due to increased uptime

- Reduced operator personnel needed

Examples of Phantom Savings

- Saving time on a job due to a new tool

- Reduction of labor without realizing any reduction in headcount

- Small reductions in energy usage

- Reduction in production machine usage to make the same output

- Reduced compressor usage due to leaks being fixed (unless you can prove electricity savings)

- Savings from reducing PM frequency

For example, consider a PM that takes 3 hours a month and does not use materials. We decided the PM was too frequent and reduced the frequency from monthly to quarterly. And let’s agree there was no increase in breakdowns or adverse events. Calculations show we “saved” 24 hours a year. Where did the savings go? We say that the time is now available for other valuable maintenance activities. This is true, but the organization won’t see it anywhere.

This is phantom savings.

- If we sent home a contractor 3 days a year due to this PM frequency improvement, the phantom savings would be realized (translated into real savings).

- If we could decrease overtime, then the savings would be realized.

- Alternatively, if the PM used a $25 belt each month and we reduced usage from 12 to 4 belts per year, we could demonstrate real savings of $200.

Real Savings and Phantom Savings are Different

We act as if the real and phantom savings are the same. They are not the same and should be thought about separately. The hard numbers people in your organization, such as accountants and finance professionals, are highly skeptical of phantom savings. Their skepticism is justified because, in the real world, the promised savings rarely materialize. Phantom savings are nice to have but are not like money in the bank.

Phantom savings are nice to have but are not like money in the bank.

This is not to say that phantom savings are insignificant; they are essential. Phantom savings can be effectively utilized for important work; the Return on Investment will be evident because of the work we do with the freed-up hours rather than the savings activity itself.

They are also a guide or a pointer to real savings. When you optimize your PM task lists, the reduction in money spent for purchases is real. Also, if the freed-up time can reduce overtime that would represent real savings also.

The Phantom Savings Trap

Consider the impact of a significant effort toward planning and scheduling the maintenance department’s workload. Conservative estimates show productivity could improve by 25%.

Typically, organizations don’t implement planning and scheduling only to lay off 25% of their people. There appears to be more work than people, so most organizations already have an excessive amount of identified work (backlog) and utilize productivity gains to accelerate the pace at which they work their way through the backlog.

Let’s analyze what is happening. Each job takes a shorter time (on the time clock) because the necessary spares, materials, tools, permissions, drawings, and equipment are available and ready for work. All the required elements of the job are available upon commencement. More jobs run smoothly, and less time is wasted.

Improved maintenance productivity doesn’t guarantee lower costs—sometimes it raises them.

While the extra work is beneficial, the “real” savings remain elusive. Without a layoff or reduction to overtime, there are no savings in maintenance costs.

To make matters worse, those additional jobs will consume parts and materials. The uptick in material usage will be genuine, not phantom. Improving productivity might adversely impact the maintenance materials budget. Imagine a successful planning and scheduling campaign causing heartburn in finance because it forces additional cash to be spent on extra parts and materials.

Because jobs are moving through the work management process more quickly, additional jobs are “discovered” that didn’t initially make it to the backlog. The jobs were pulled in from limbo as no one had confidence that the job would ever be completed. This is particularly true for infrastructure jobs.

There Will Be Real Savings

Eventually, when the backlog is reduced to a manageable level, the entire plant will run more efficiently. A couple of things might produce real savings:

- Time for RCA so we can reduce the number of repetitive problems

- Time for defect elimination

- Reduction in overdue PMs

- Time for Small Improvement Projects

- Fewer corrective jobs will break down while waiting for maintenance to schedule the work.

Keep in mind the difference.

Finally, I wish the esteemed vendors in our industry would be more rigorous in talking about savings. Maybe we could start a dialog about the right ways to discuss savings from their product,